Saturday, February 1, 1969

Allen Klein, John Eastman, and The Beatles discuss about NEMS

Last updated on August 19, 2025

Saturday, February 1, 1969

Last updated on August 19, 2025

Film Jan 31, 1969 • Shooting of "Let It Be" promo film

Article Early February 1969 • Paul and Linda have lunch at the London Post Tower

Article Feb 01, 1969 • Allen Klein, John Eastman, and The Beatles discuss about NEMS

Session February 1969 • Home recording • Goodbye

Session Early February 1969 • Recording "Rosetta"

Next article Feb 03, 1969 • Allen Klein appointed to look into The Beatles' affairs

Fall 1968 • Apple faces business problems

January 1969 • Apple's business problems become public knowledge

Jan 12, 1969 • The Beatles meet together to discuss their personal and business problems

Jan 27, 1969 • Allen Klein meets with John Lennon

Jan 28, 1969 • Allen Klein meets with The Beatles

Feb 01, 1969 • Allen Klein, John Eastman, and The Beatles discuss about NEMS

Feb 03, 1969 • Allen Klein appointed to look into The Beatles' affairs

January to February 17, 1969 • NEMS / Nemperor is sold to Triumph Investment Trust

February 21 to August 1969 • The Beatles fight for NEMS / Nemperor

March 1969 • Dick James sells his Northern Songs shares to ATV

Mar 21, 1969 • Allen Klein becomes business manager of Apple

April - May 1969 • The Beatles and ATV fight for the control of Northern Songs

September to November 1969 • ATV finalizes its acquisition of Northern Songs

Apple Records is officially launched

Aug 11, 1968

Fall 1968

Apple publishes its first internal magazine

November 1968

Jan 01, 1969

Installation of Apple recording studio at 3 Savile Row

January 17-19, 1969

Allen Klein becomes business manager of Apple

Mar 21, 1969

Apple Corps’ first annual board meeting

Aug 21, 1969

The Beatles sign the new Capitol / EMI agreement

Sep 20, 1969

Rumours of Apple’s acquisition surface

Aug 06, 1971

By the fall of 1968, it had become clear to Apple’s management team – and consequently to The Beatles – that the company was hemorrhaging money and the situation was becoming unsustainable. As a result, the search for a new manager began. Paul McCartney quickly came to believe that Lee Eastman, father of Linda Eastman and his future father-in-law, should take control of The Beatles’ financial affairs. While John Lennon, George Harrison and Ringo Starr were uneasy with the idea of Paul’s future in-laws managing the group’s business, in January 1969, they agreed to appoint Lee Eastman and his son John Eastman as temporary business advisors.

Shortly after, John Eastman proposed the idea of acquiring Brian Epstein’s former company, NEMS Enterprises, for £1 million. Meanwhile, on January 27, John Lennon appointed the controversial American businessman Allen Klein as his personal adviser.

I saw Clive Epstein immediately. I told him, ‘Look, you can’t get the money out of the company to pay estate taxes, so why don’t we buy NEMS and you’ll get the money as a capital gain. Forget the twenty-five per cent (NEMS’ entitlement of Beatles’ royalties). What’s the company worth? Eight-hundred-thousand pounds? Nine-hundred-thousand pounds? Forget it, we won’t quibble, we’ll give you a million!

John Eastman – From “The Beatles: Off the Record” by Keith Badman, 2008

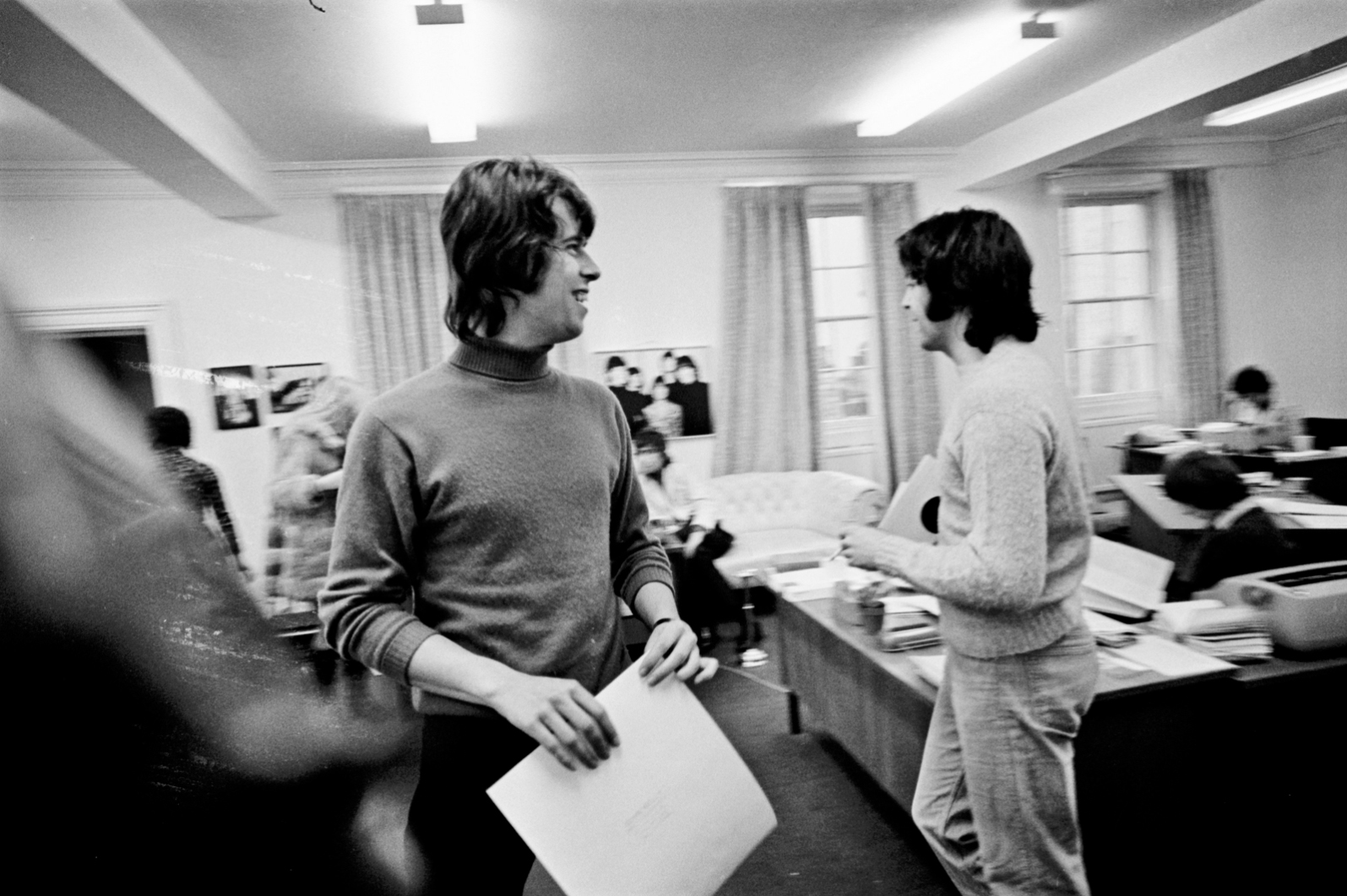

Following an initial meeting between Klein and all four Beatles on January 28, they reconvened on this day, February 1, to further discuss the proposed acquisition of NEMS, as presented by John Eastman.

The following excerpt is taken from Allen Klein’s affidavit, read aloud at the High Court in London during Paul McCartney’s 1971 lawsuit to dissolve The Beatles’ partnership:

The purpose of the meeting on 1st February was, as I have indicated, primarily to discuss the proposed acquisition of NEMS. John Eastman was proposing this on two grounds: first, that it was a good deal in any case, because the company was available for £1 million and in itself was worth £1 million, and that the money in the Company could be used to pay for the purchase. (I did not know at that time that there was anything unlawful in such an arrangement, but I did know that in order to have £1 million to spend you have to earn a considerably larger sum before tax, and if the advance of £1 million from EMI to fund the purchase was going to have to be paid back out of royalty income, I explained that earnings of at least £2 million would be required.) The second ground on which Eastman recommended the purchase was that NEMS owned a block of 237,000 shares in Northern Songs Limited (“Northern Songs”). Northern Songs was a Public Company quoted on The Stock Exchange, London. Its principal assets were rights, derived from Maclen (Music) Limited. (“maclen”), in the compostitions of Mr Lennon and the Plaintiff, including future compositions until February 1973.

At this meeting (1st February 1969) the Plaintiff [Paul McCartney] introduced the subject of Northern Songs and said that he wanted The Beatles to own it. I suggested that it was something that we could look at later. As regards the large holding of NEMS in Northern Songs, I said that at that time I did not feel that the existence of the holding was a sufficient reason to pay £1 million out of a company (Apple) when we did not know what its financial position was. It was agreed that the idea of buying the share capital of NEMS and the possible acquisition of Northern Songs should be shelved until the financial position of The Beatles’ companies had been ascertained and it was also agreed by all four Beatles that I should be persuaded to look into the financial position of those companies.

At this stage John Eastman launched an attack on my personal integrity, producing a copy of the Cameo-Parkway Proxy Statement mentioned above and clippings from newspapers. He alleged that I had a bad reputation in general and raised questions about Cameo-Parkway in particular. I pointed out that the Cameo-Parkway Proxy Statement made, in accordance with the stringent requirements of United States law and practice with respect to securities transactions, a full and complete disclosure of the “warts” of Cameo-Parkway’s career and was there for all to see. I also invited him to make specific charges or criticisms which would enable me to answer them, but he did not do so. In any case I think that my answers must have satisfied The Beatles. I suggested that the position of John Eastman should be that of legal adviser to The Beatles and all their companies. He rejected this on the ground that he did more than an English lawyer normally does. the meeting broke up and another meeting was arranged for the following Monday 3rd February 1969, again at Saville Row.

Allen Klein – From beatlesbible.com

The attempt to buy NEMS Enterprises ultimately failed. Instead, NEMS was sold to Triumph Investment Trust on February 14, 1969.

The Beatles Diary Volume 1: The Beatles Years

With greatly expanded text, this is the most revealing and frank personal 30-year chronicle of the group ever written. Insider Barry Miles covers the Beatles story from childhood to the break-up of the group.

If we modestly consider the Paul McCartney Project to be the premier online resource for all things Paul McCartney, it is undeniable that The Beatles Bible stands as the definitive online site dedicated to the Beatles. While there is some overlap in content between the two sites, they differ significantly in their approach.

Notice any inaccuracies on this page? Have additional insights or ideas for new content? Or just want to share your thoughts? We value your feedback! Please use the form below to get in touch with us.